Given all of the recent market volatility it seems like the one certainty is that it is uncertain how these forces will play out in both the short and long term.

The charts here mostly reflect market conditions that predate the most dramatic recent financial developments (there is typically a 3 to 6 week time lag between deals being made, i.e. listings going into contract, and sales closing escrow). The impacts of the broader economic climate will come into better focus in the coming weeks and months.

Generally speaking, in San Francisco and the Bay Area, sales volume and overbidding typically increased, and homes sold more quickly. The quantity of new and active listings rose across the Bay Area, sometimes very substantially, with growing impact on supply and demand dynamics – and price reductions increased as well.

From my perspective in our corner of the globe, the spring market has been busy. I’m seeing good attendance at open houses, and plenty of buyer interest and multiple offers for well-priced properties.

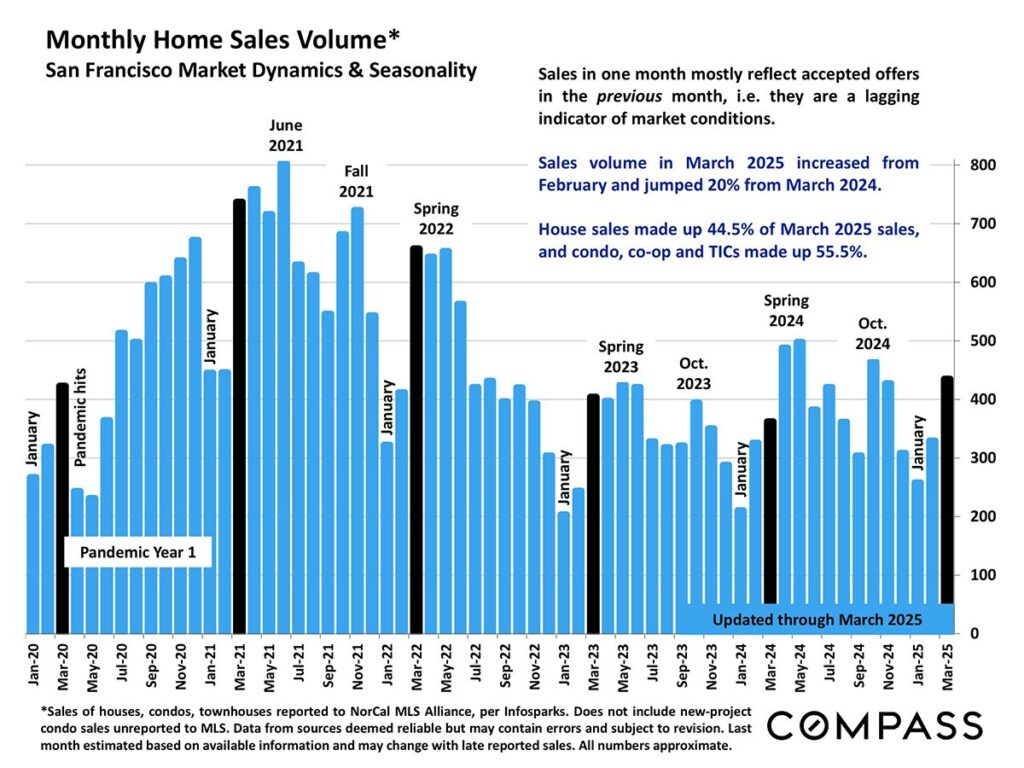

Home Sales Volume

Sales volume in March 2025 increased by 20% from March 2024. House sales accounted for 44.5% of sales and condos, co-ops, and TICs made up 55.5%.

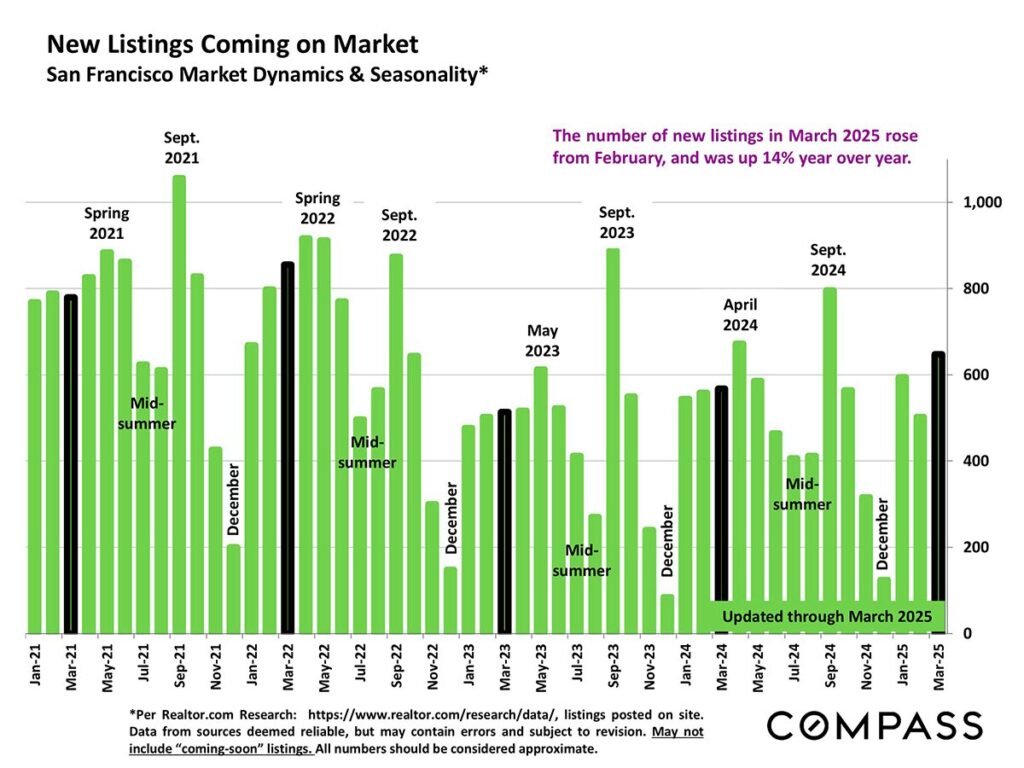

New Listings

The number of new listings coming on the market in March 2025 was up 14% compared to March 2024.

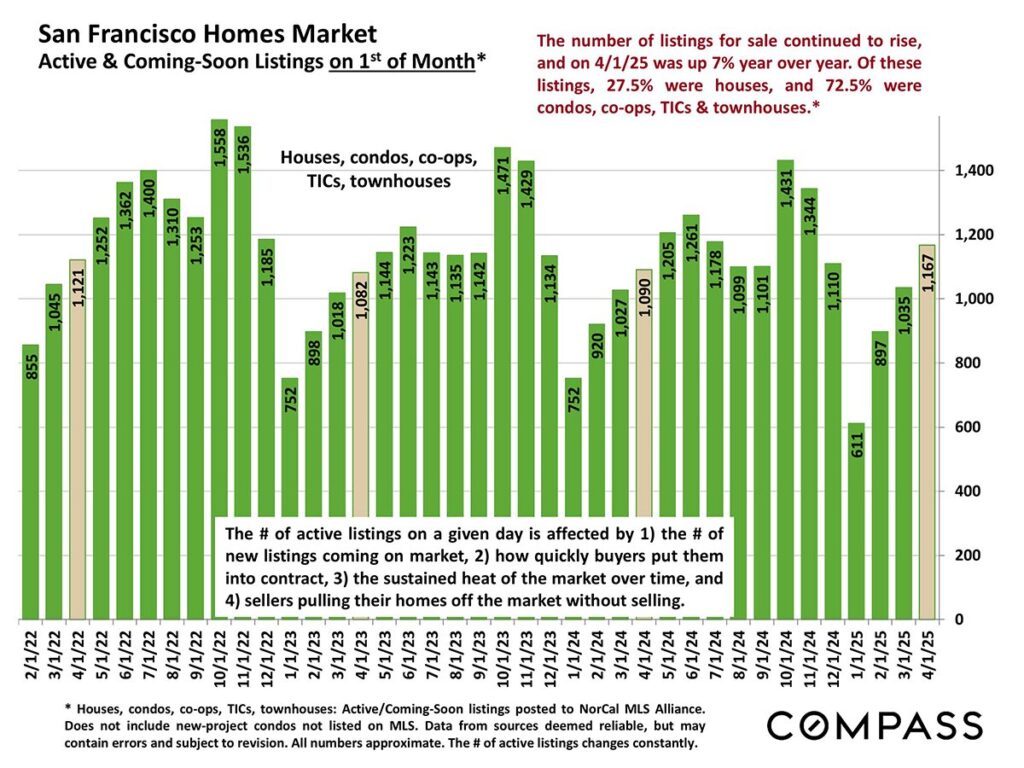

Active and Coming Soon Listings

The number of active and coming soon listings on the first day of April 2025 was up 7% compared to April 2024. 27.5% of these listings were houses and the remaining were condos, co-ops and TICs.

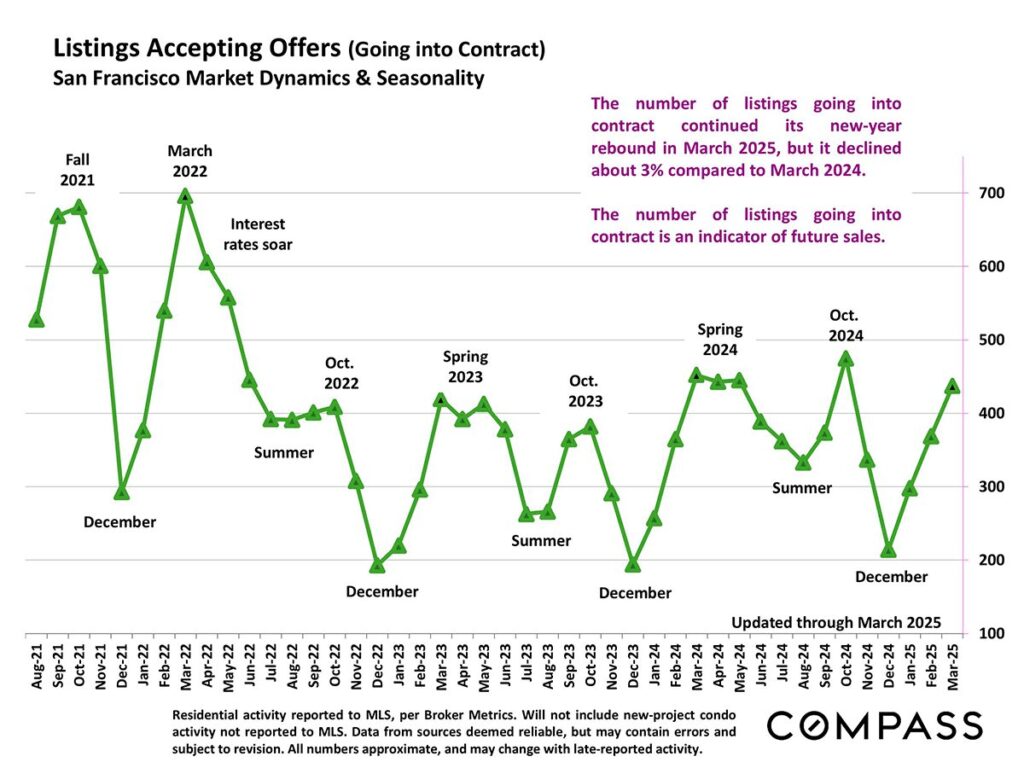

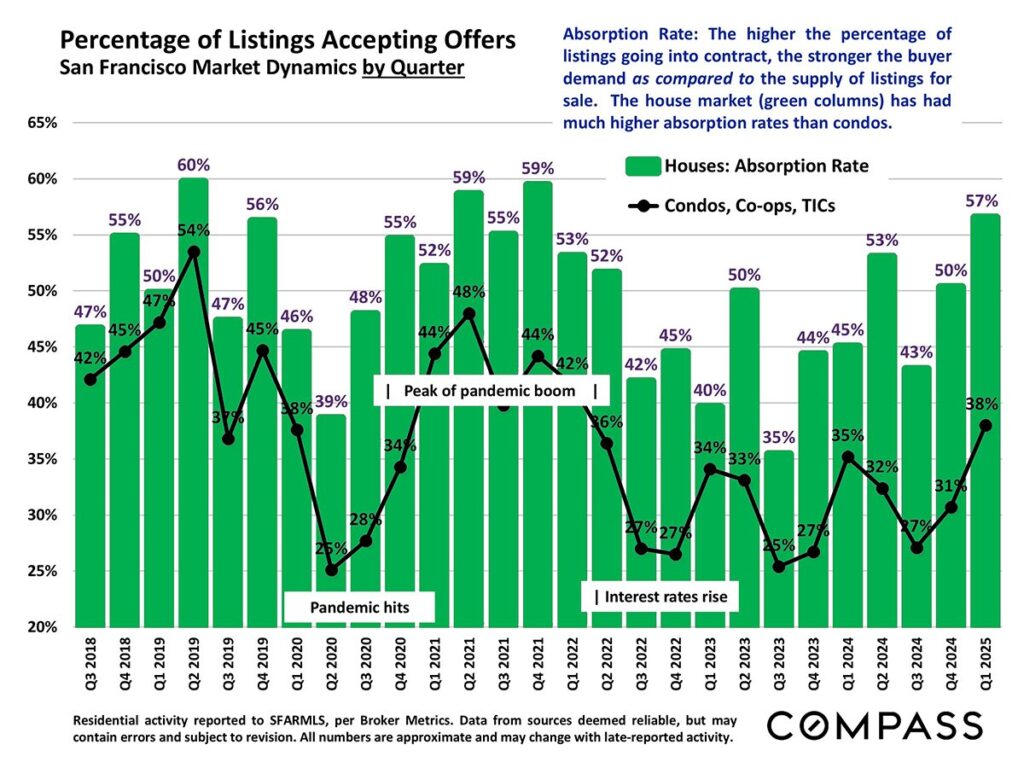

Listings Accepting Offers

The number of listings going into contract rebounded in March 2025, but was about 3% lower than in March 2024.

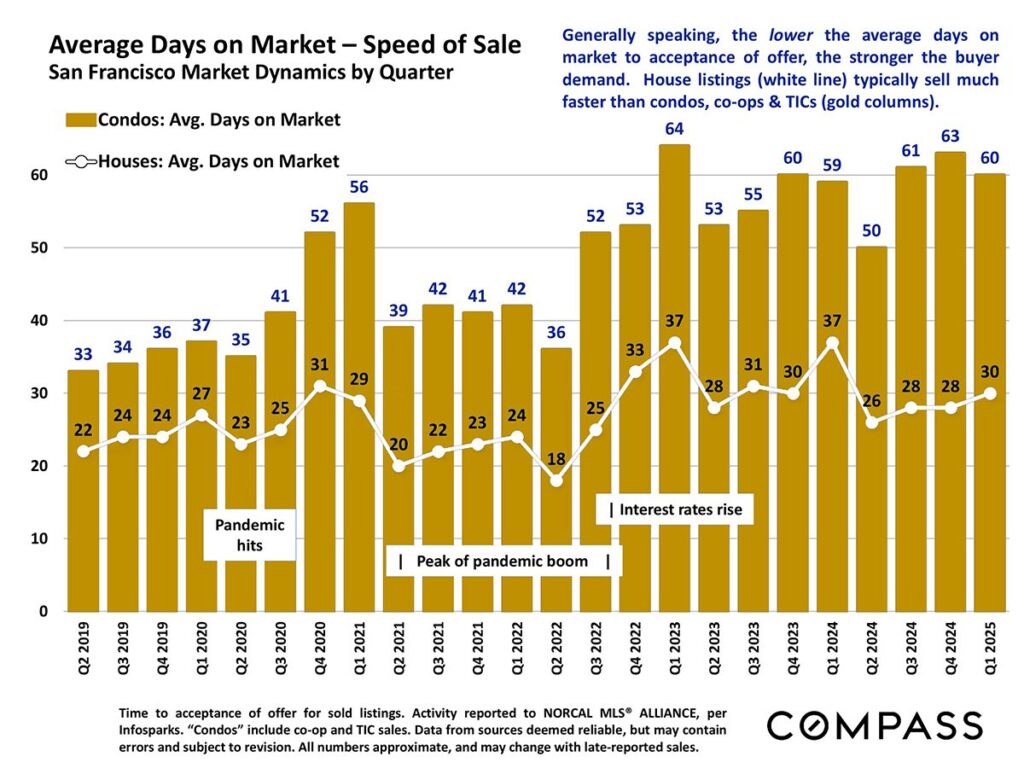

Average Days on Market

The average days on market in the first quarter of 2025 (30 days) was 21% lower than in the first quarters of 2024 and 2023 (37 days).

Listings Accepting Offers

Houses continue to have a much higher absorption rate than condos. The 2025 Q1 rate is higher than in 2024 and 2023.

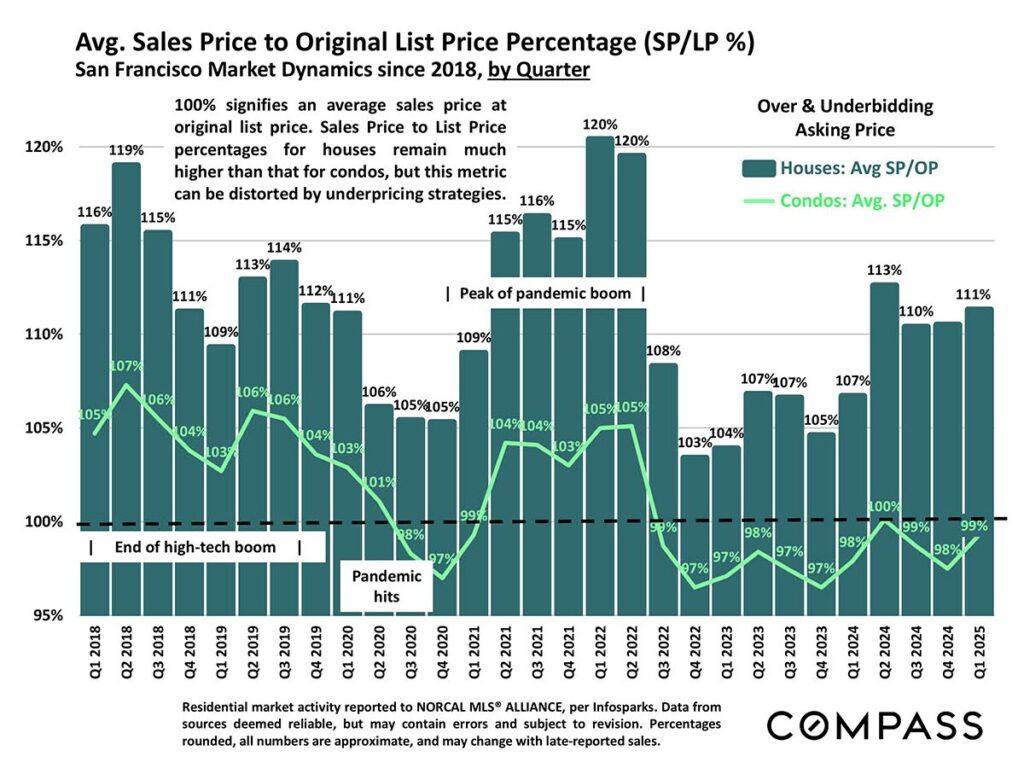

Sales Over List Price

Houses continue to outperform condos in sales over list price. In Q1 2025, houses averaging 111% over list, while condos averaged 99% of list price.

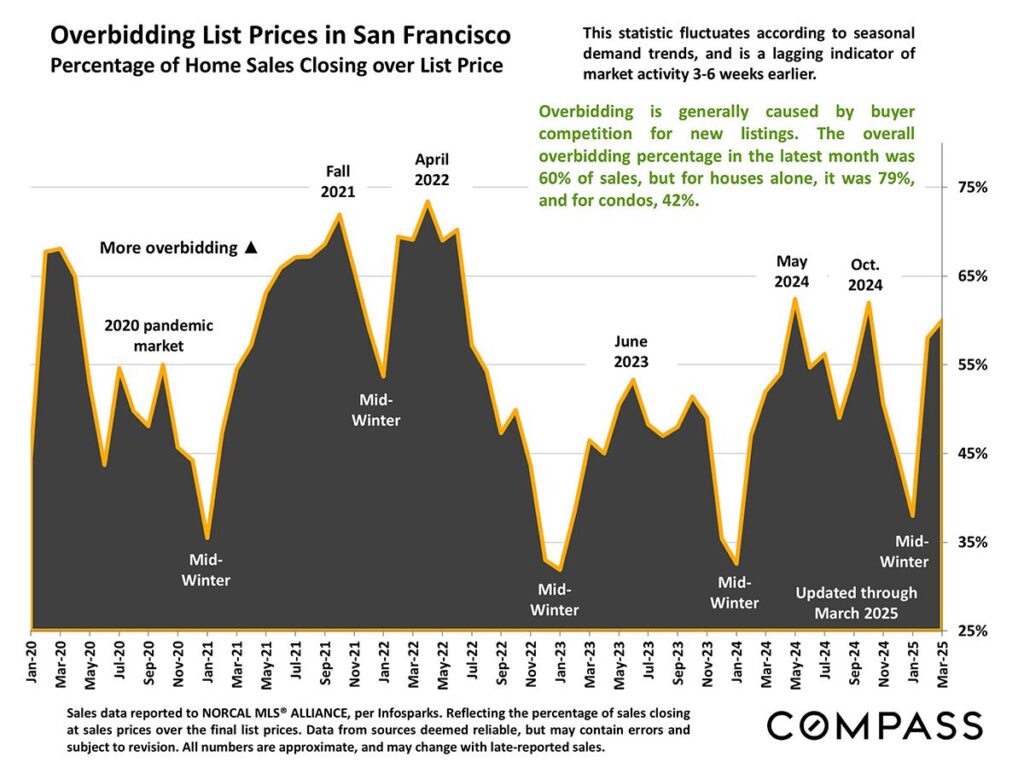

Overbidding List Prices

The overall overbidding percentage in March 2025 was for 60% of sales, but for houses alone it was 79%. For condos, it was 42%.

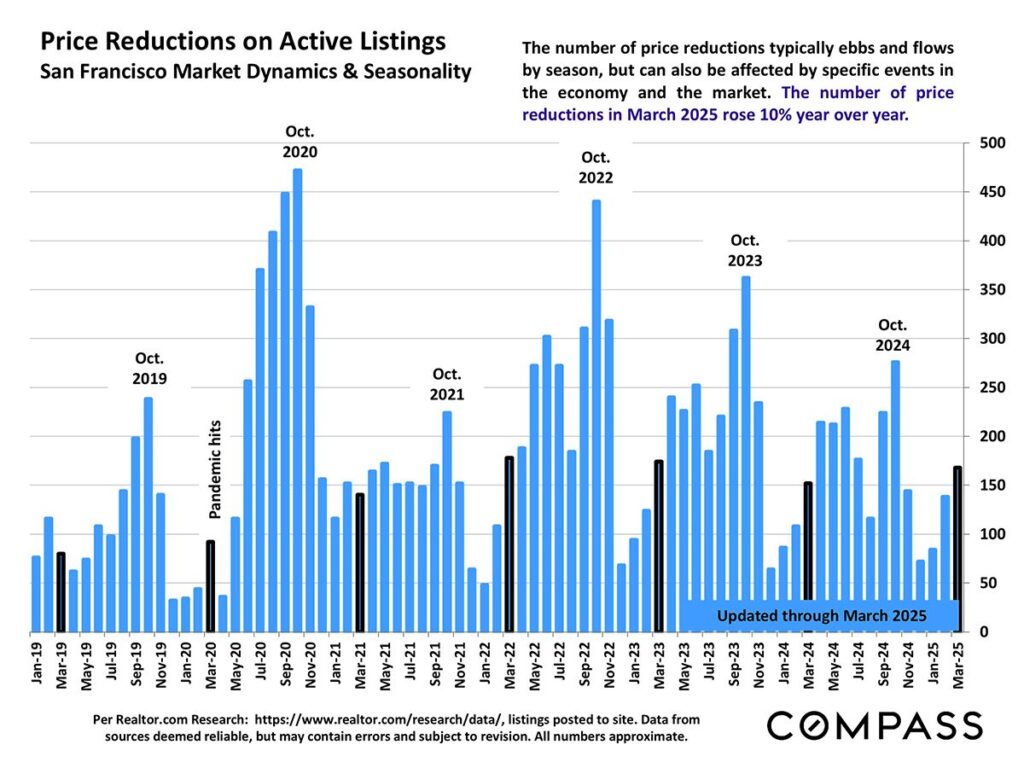

Price Reductions on Active Listings

The number of price reductions in March 2025 rose 10% compared to March 2024.

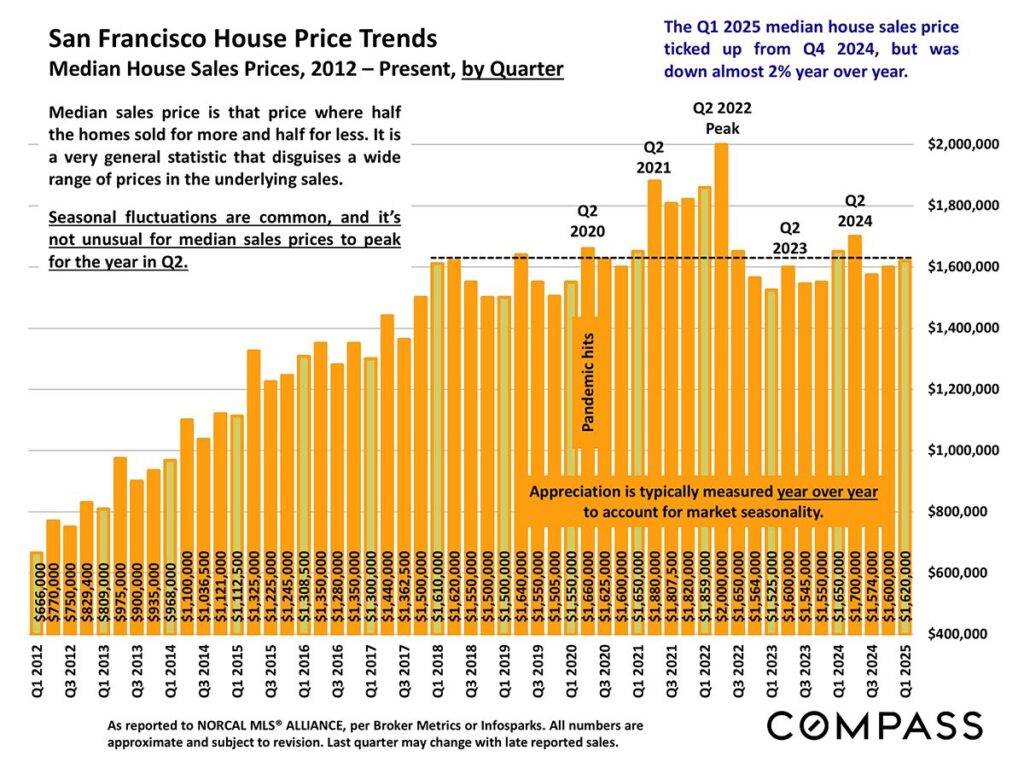

House Price Trends

The Q1 2025 median house sales price was down almost 2% from Q1 2024.

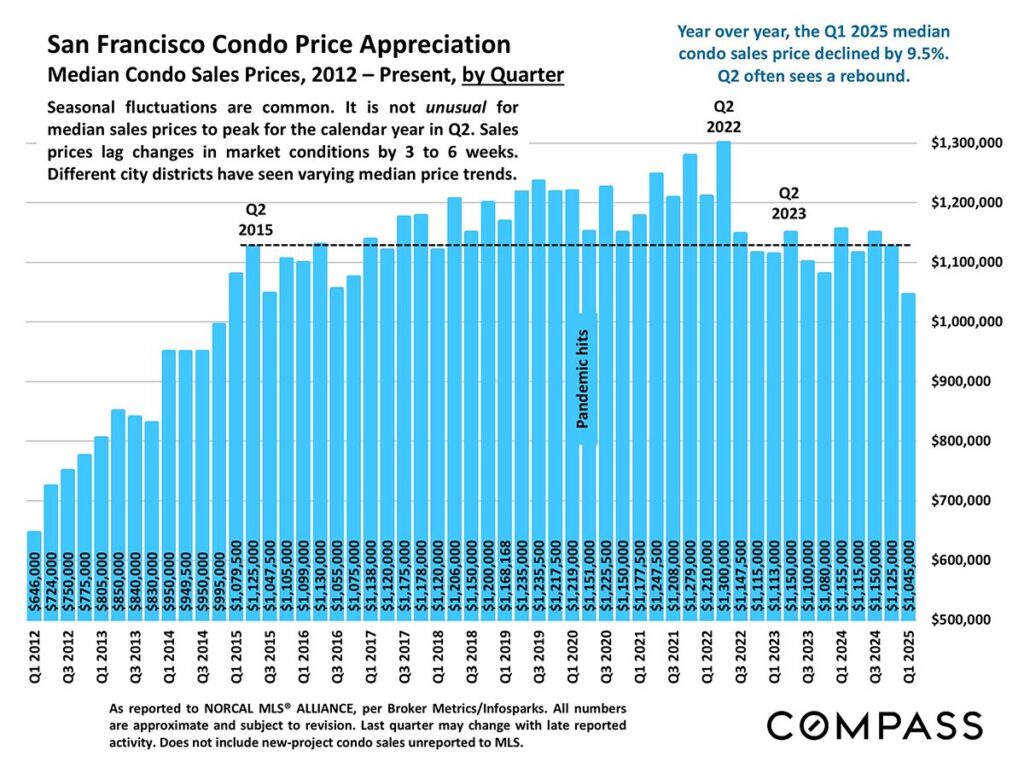

Condo Price Appreciation

The Q1 2025 median condo sales price declined by 9.5% compared to Q1 2024.

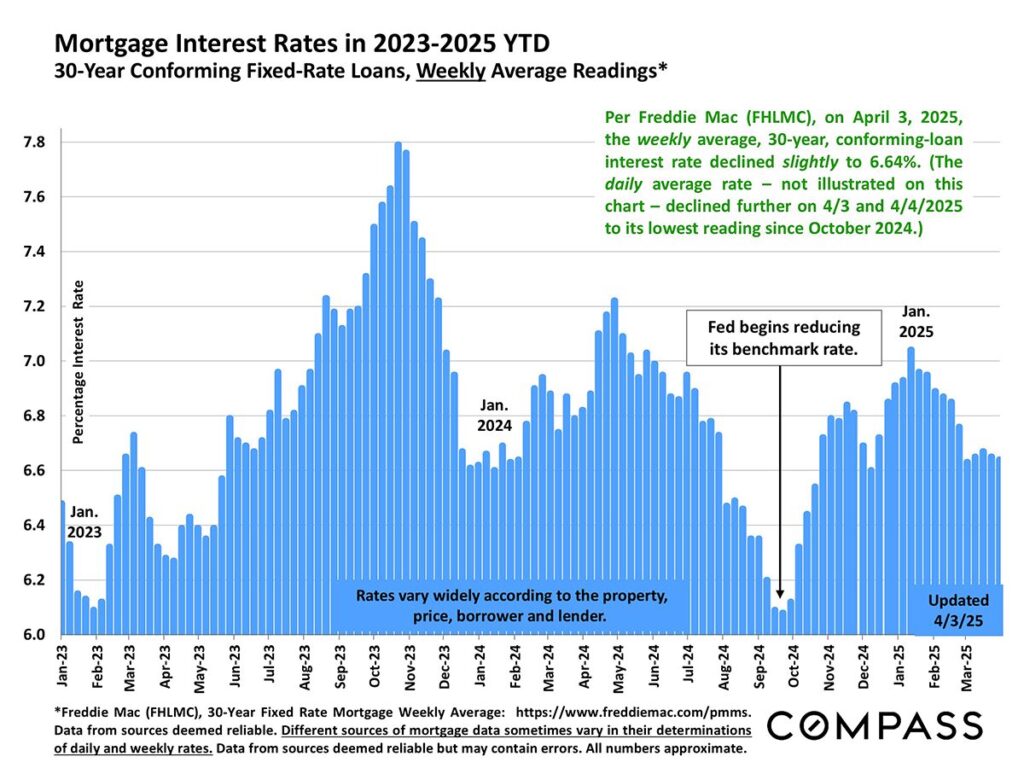

Mortgage Rates

As of April 3, 2025, the 30-year fixed-rate mortgage interest rate declined slightly to 6.64%. On the heels of tariff announcements, rates were pushed higher; but, as of April 15, the average 30-year fixed rate was just below 7%. Rates will continue to respond to market volatility with ongoing tariff changes and fluctuations in consumer confidence.

The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information.