After the decline in market activity in the second half of 2022, buyer demand rebounded dramatically and most market indicators turned positive in early 2023. Open house traffic, offers, and overbidding and absorption rates all saw substantial improvement.

Even so, most year-over-year indicators remain depressed, but these comparisons are to the severely overheated conditions prevailing at the peak of a 10-year housing market upcycle. Over the last 3 years, spring markets were deeply affected, in very different and sometimes unusual ways, by the onset of the pandemic (2020), the pandemic boom (2021), and soaring interest rates (2022).

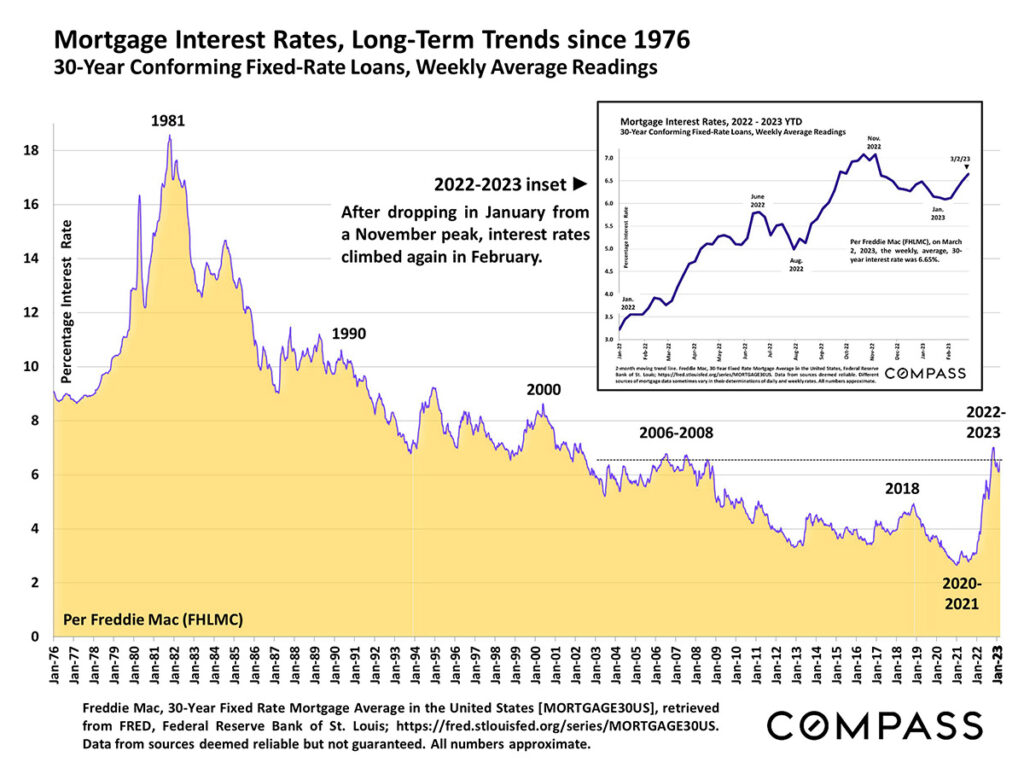

As has been the case for the last 14 months, the biggest wildcard remains interest rates. After dropping considerably in January from a November peak, rates climbed again in February.

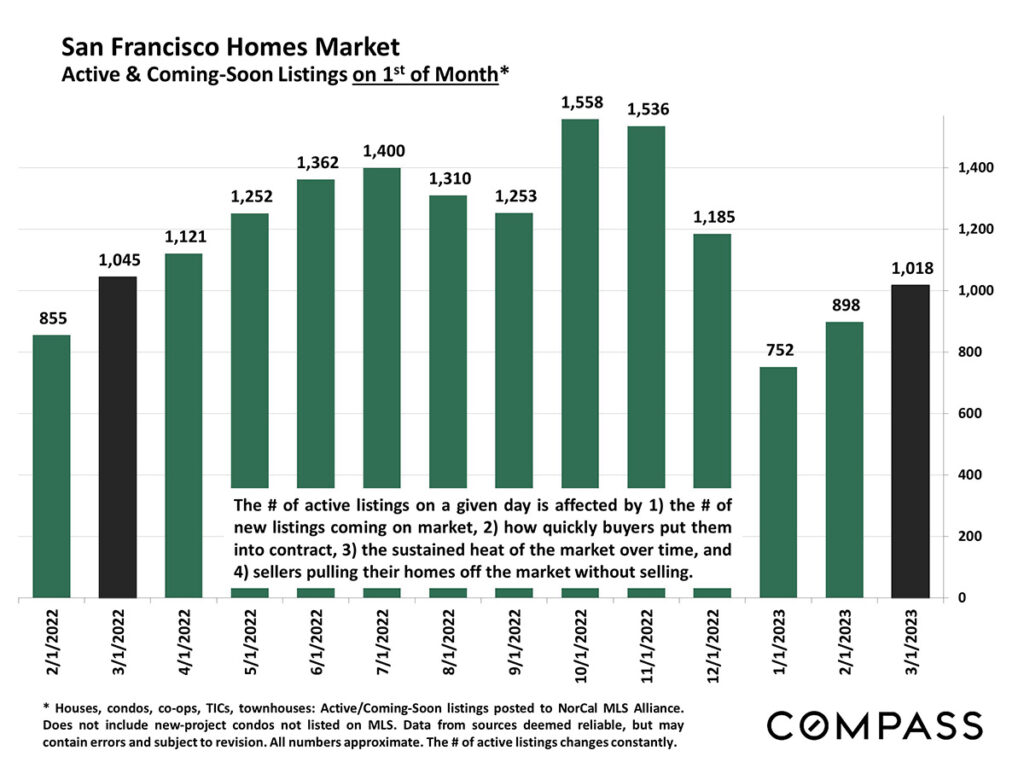

March through May is typically the most active listing and sales period of the year, and should soon provide much more data on supply, demand and price trends.

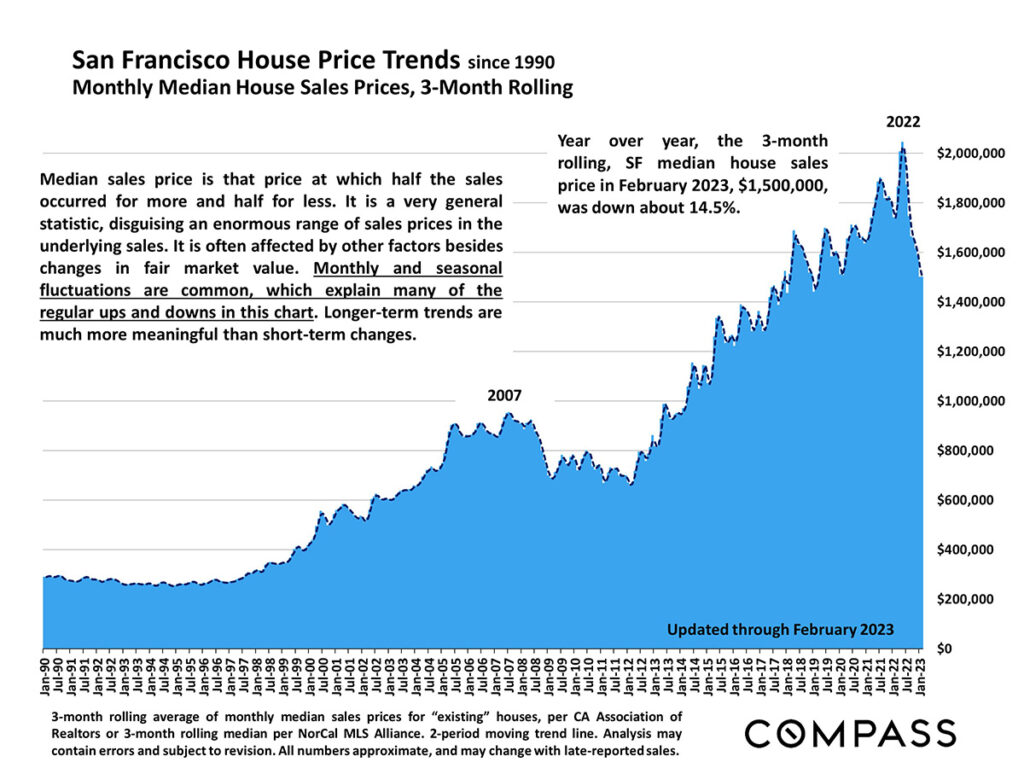

House Price Trends

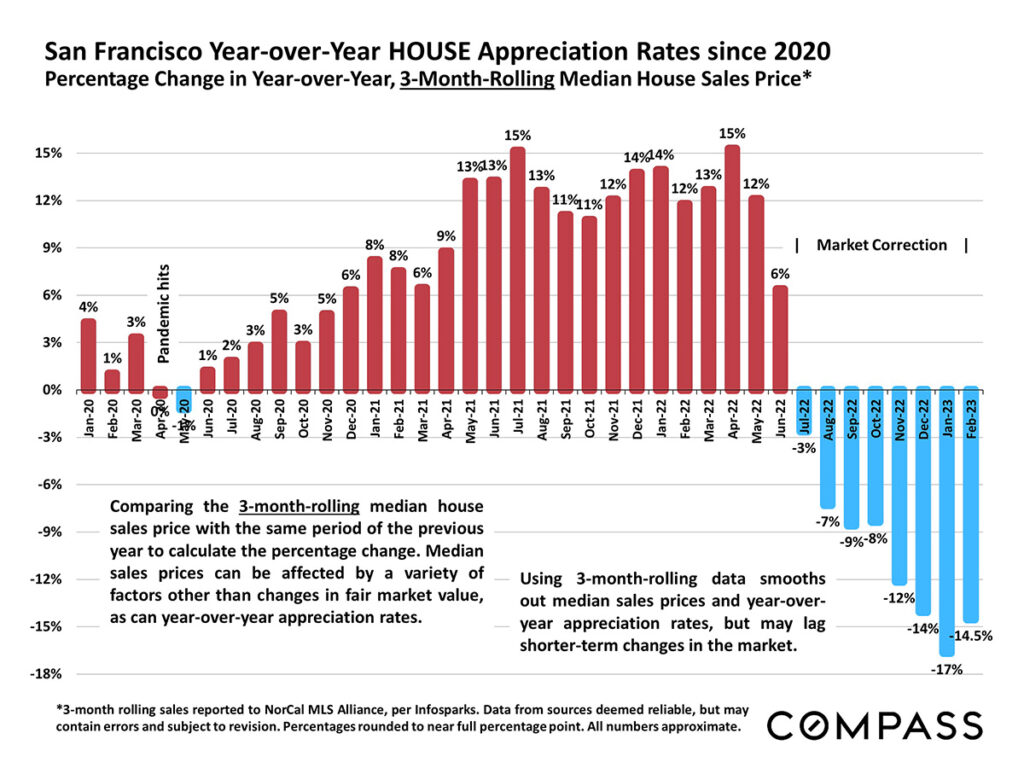

Year over year, the median house sales price in February 2023 was down about 14.5%.

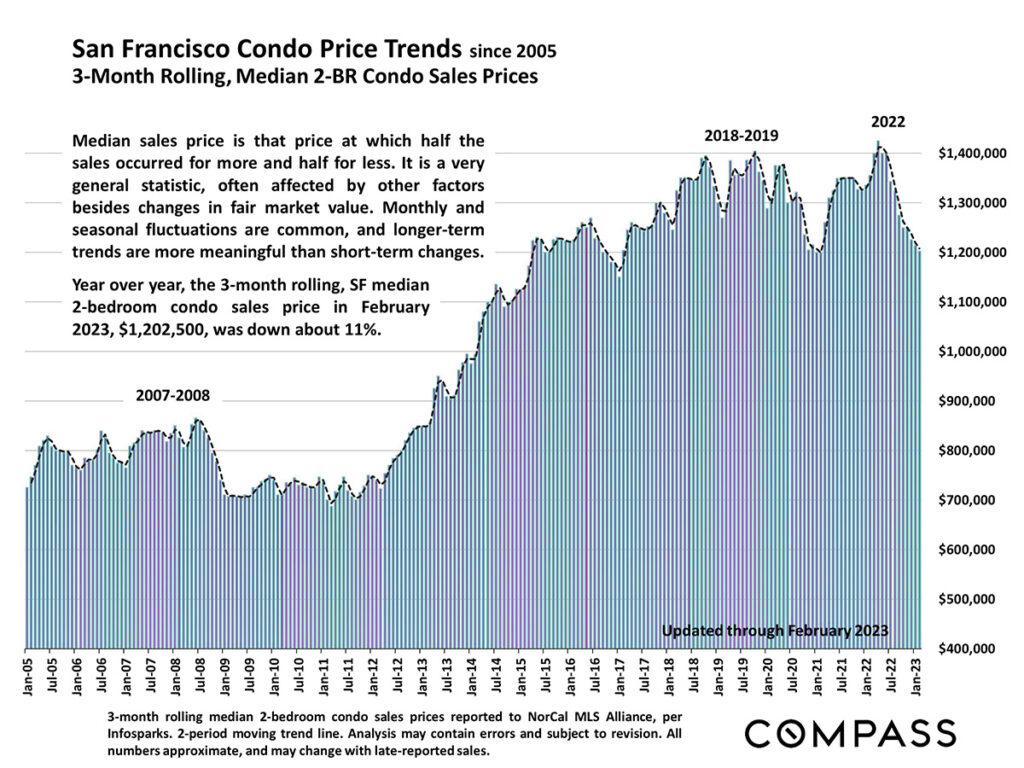

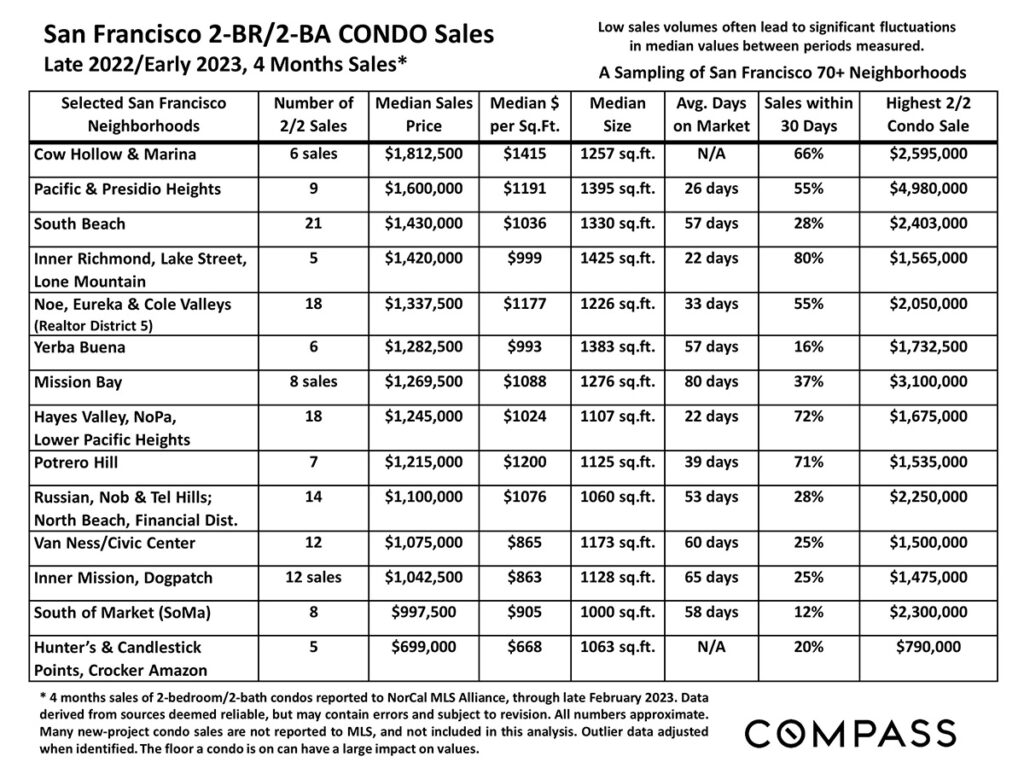

Condo Price Trends

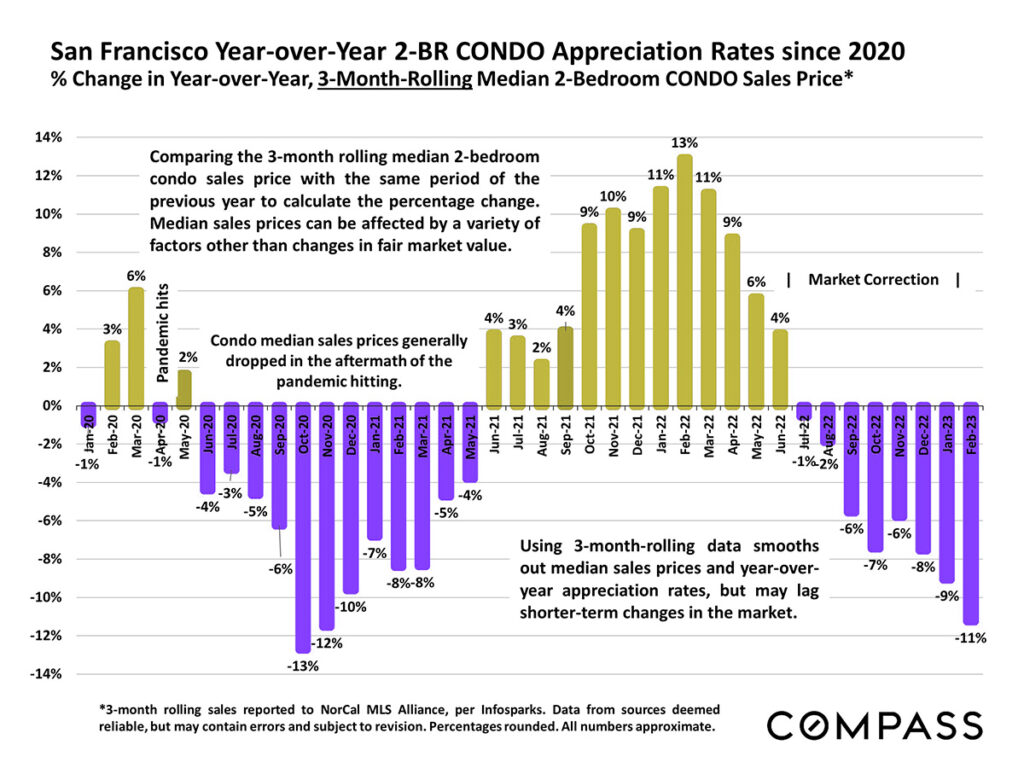

Year over year, the median sales price for a 2-bedroom condo in February 2023 was down about 11%.

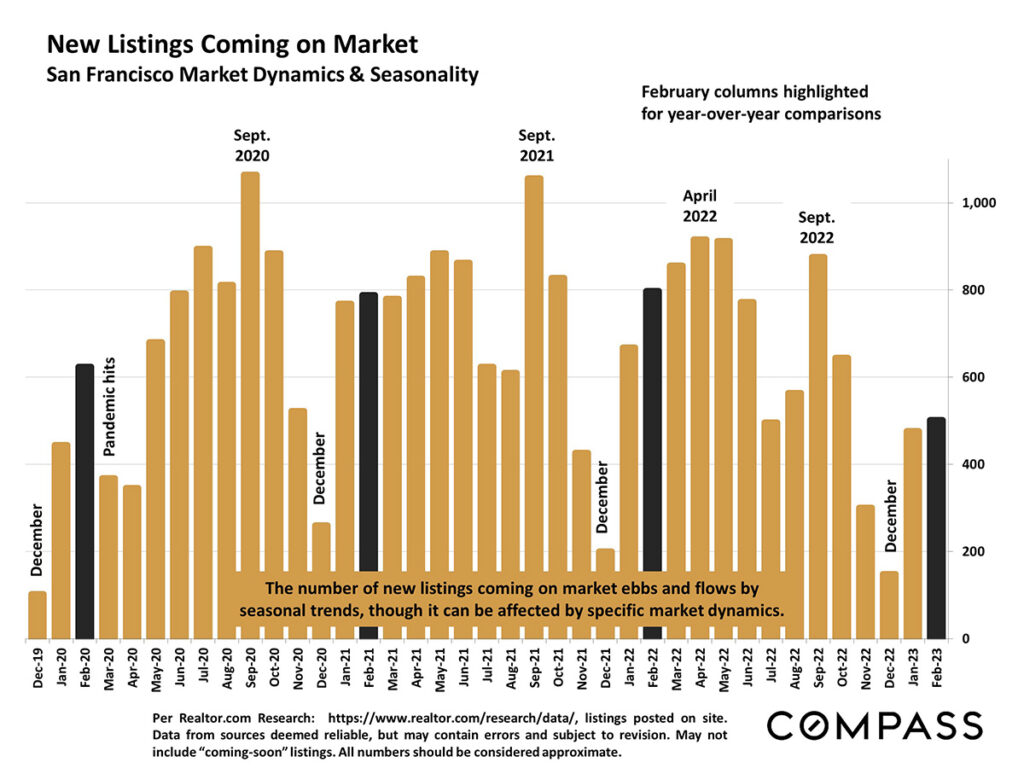

New Listings Coming on Market

In the chart below, the columns in black show year-over-year comparisons of new listings on the market in February.

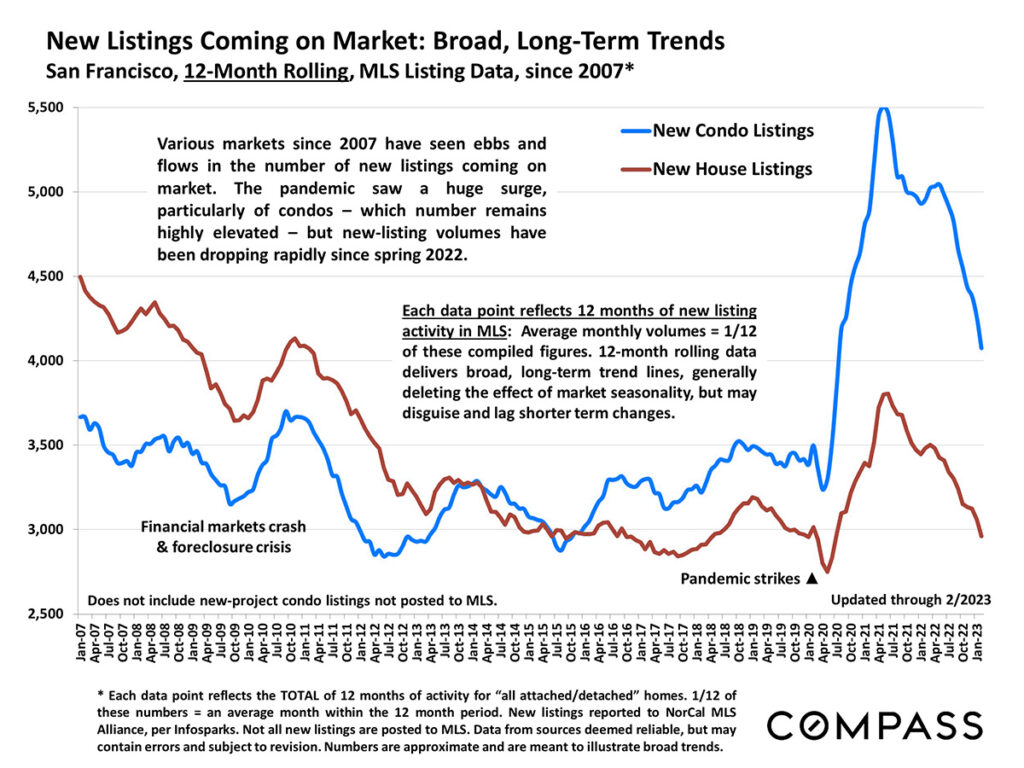

In the wake of the pandemic, condo listings surged to historic levels, but have been dropping rapidly since the spring of 2022.

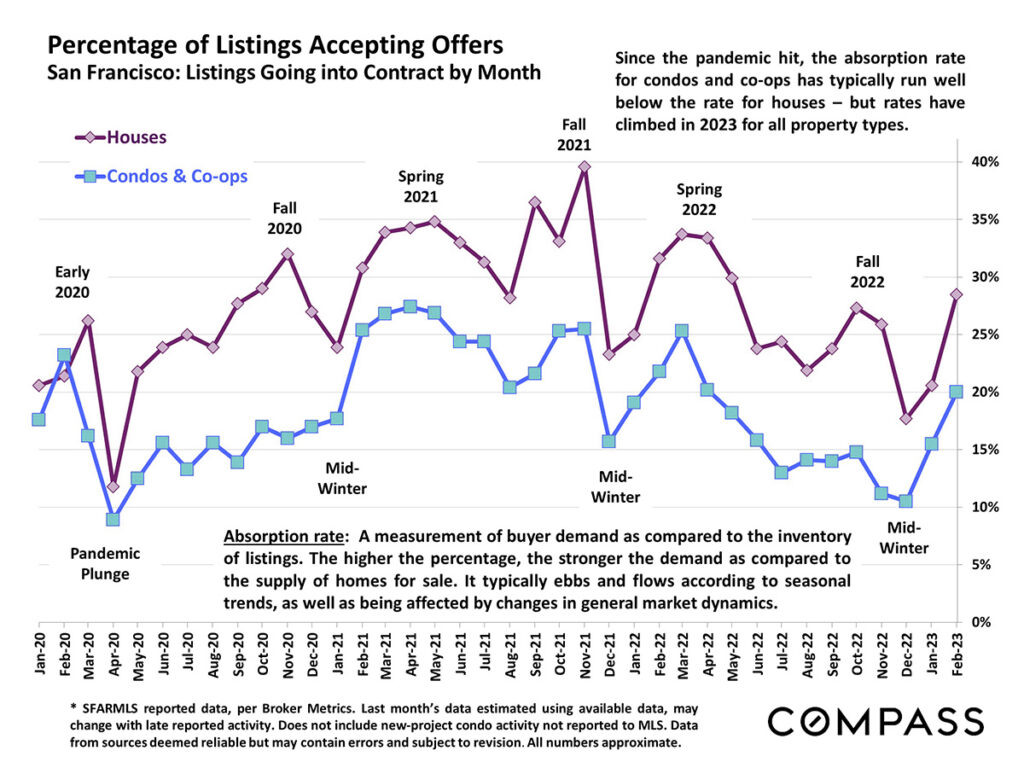

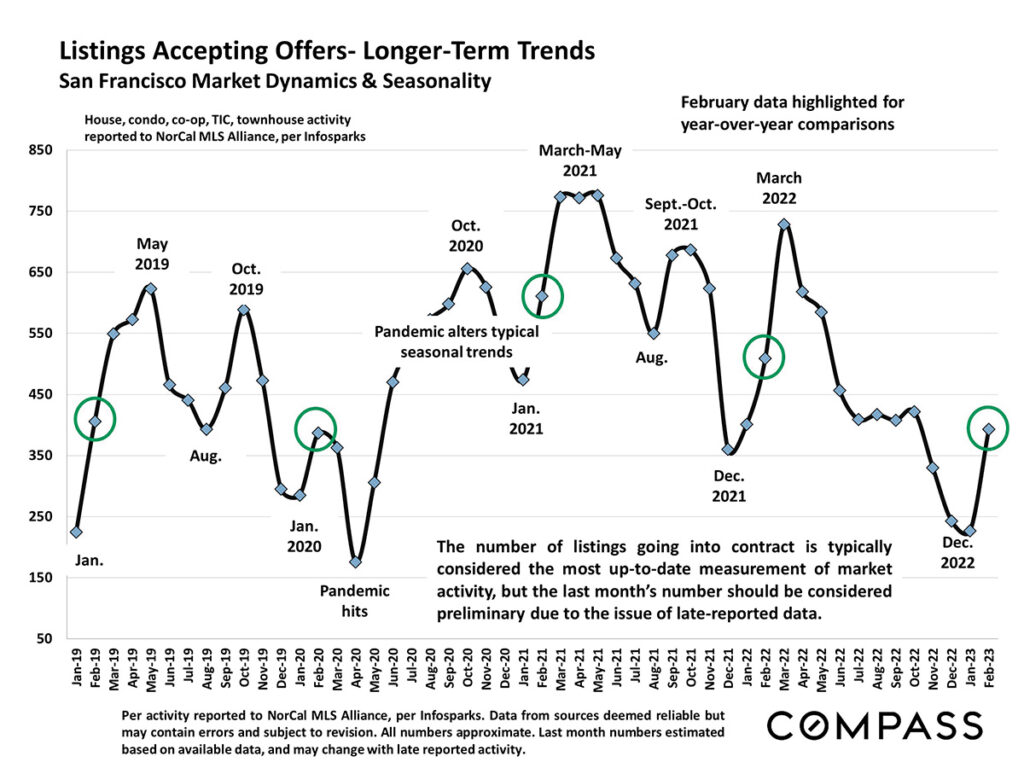

Listings Accepting Offers

Absorption rate shows buyer demand compared to the inventory of listings on the market. While the absorption rate for condos and co-ops typically runs below the rate for houses, the rates for both have climbed in 2023.

The number of listings accepting offers in February 2023 was similar to February 2020, right before the pandemic hit.

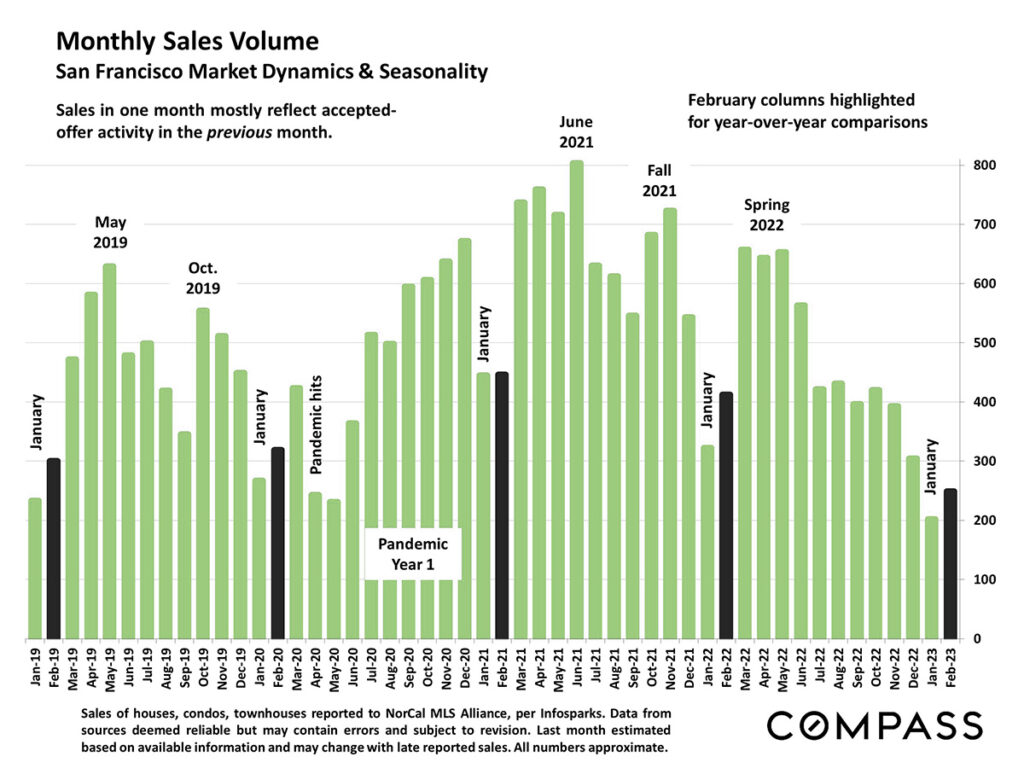

Monthly Sales Volume

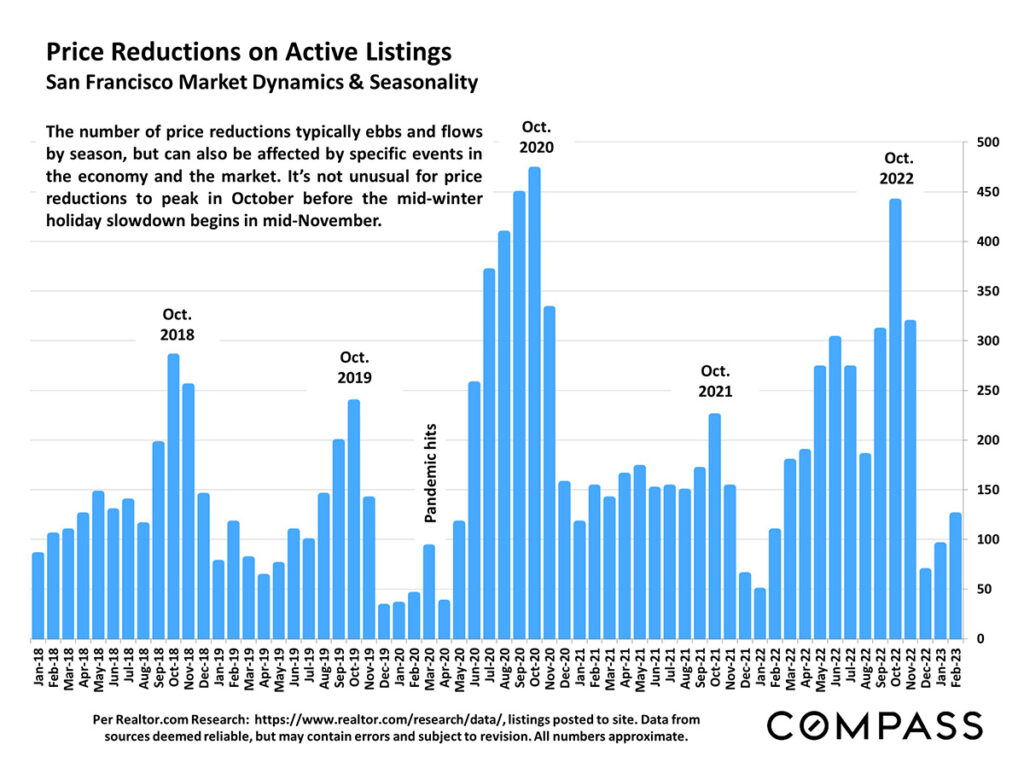

Price Reductions on Active Listings

Sales Over List Price

Average Days on Market

In general, houses have a much lower average days on market than condos, but both have dropped from their highs in January 2023.

Mortgage Interest Rate Trends

At the start of 2023, the 30-year fixed-rate mortgage decreased with expectations of lower economic growth, inflation and a loosening of monetary policy. Given sustained economic growth and continued inflation, mortgage rates are now inching up toward seven percent.

The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information.